The bank tried to take his farm for $50,000. They had lawyers, documents, a court date already set. And for 3 weeks, it looked like they were going to win. But they missed one detail. Every month for 22 years, they sent him the same statement. And in those numbers, one number was off. Raymond Holt saw it.

And that one mistake is why the bank didn’t take his farm. They ended up owing him $1.2 million instead. Raymond Holt was 68. And for 22 years, he had been paying the same farm loan. Every single month for 22 years. And he paid it all to the same place, First Continental Rural Bank.

A small local bank his family had trusted for generations. Raymond trusted them, too. That turned out to be a mistake. Because while Raymond was making those payments, he was also doing something most people don’t. He was actually looking at the numbers. And after 22 years of reading those statements, he noticed a charge that shouldn’t have been there.

The letter wasn’t waiting on his kitchen table. It was in the mailbox at the end of his driveway. Raymond saw the bank’s logo and stopped. He opened it, read the first line, then read it again. Slower this time. Making sure he wasn’t reading it wrong. The bank said he owed $50,000. Payment discrepancies. A balance they said had been growing for years.

And under his loan terms, the land itself was collateral. 240 acres. His home. His entire life. And all of it on the line. For a debt he never agreed to owe. He had 30 days to respond. Just 30 days. Raymond called the bank from the roadside. 18 minutes on hold. When someone answered, they were calm, professional. They confirmed the balance, the deadline, and said if nothing changed, foreclosure would begin automatically.

Automatically. Like 22 years of payments meant nothing. Raymond lowered the phone and looked back at his land. Then he called his son, Daniel. Daniel listened. Then said, “Dad, how is that even possible?” Raymond said, “That’s what I’m trying to figure out.” “You need a lawyer. Not the bank you own today.” “I know.

” But here’s what neither of them said. $50,000 wasn’t the number bothering Raymond. It was another number. One he had noticed 3 weeks earlier on his January statement. A number that had been there every month for years. He ignored it before. Now, he couldn’t. What was that number? And why had the bank never mentioned it? That question is about to become the bank’s worst mistake. Her name was Sandra Cole.

She was 52 and had spent 27 years handling property and banking cases in Kentucky courtrooms. She was the kind of lawyer who didn’t speak unless she was certain. She came to Raymond’s farmhouse the next morning, sat down, and read the bank’s letter from start to finish. Then she looked up and asked him three questions.

How long had he been making payments? Had the bank ever mentioned discrepancies before this? And did he still have his monthly statements? Raymond answered immediately. 22 years. Never. And yes, every single one. The statements were in a folder in the bottom drawer of his desk. Sandra told him to bring it. Raymond placed the folder on the table.

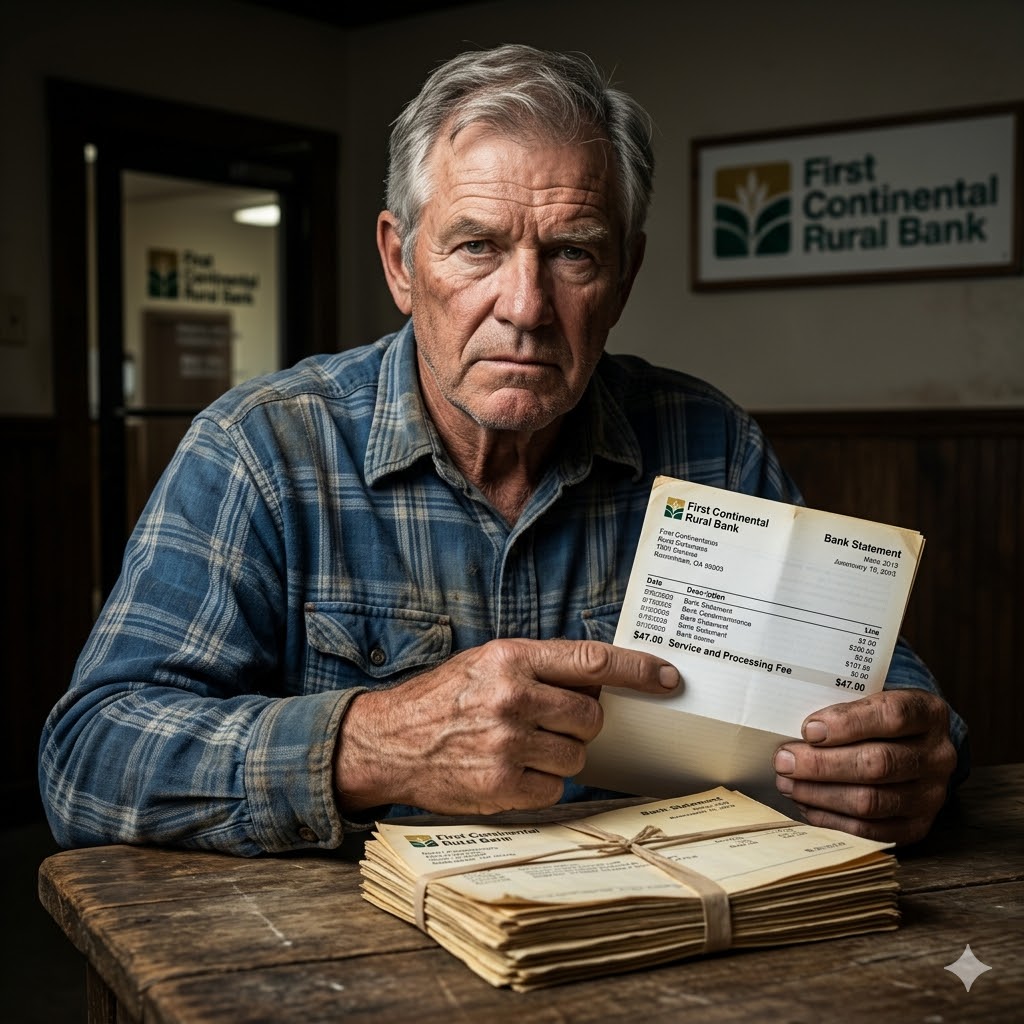

Inside were over two decades of records. Every payment. Every statement. Every detail the bank had ever sent him. Sandra opened it and started going through them one by one. Reading carefully. She didn’t rush. And she didn’t comment. A few minutes later, she paused. She picked up one of the statements again and looked at it more closely.

Raymond noticed. “What is it?” Sandra pointed to a line near the bottom of the page. A charge, $47, labeled service and processing fee. Raymond glanced at it. “That’s always been there.” Sandra didn’t look up. “Every month?” “Every month.” Raymond said. “For as long as I can remember.” Sandra set the statement down and reached for the original loan agreement.

She went through the section on fees, then checked it again. Slower this time. When she looked up, her expression had changed. “Raymond, this fee isn’t in your loan agreement. It’s not listed anywhere in your contract.” Raymond frowned. “What does that mean?” Sandra held his gaze. “It means the bank has been charging you $47 every single month for 22 years for something they were never allowed to charge.

” The room went quiet. Raymond looked back at the statement. “So they’ve been overcharging me?” Sandra nodded. “Yes. And that’s just what we can see so far. Because $47 a month doesn’t sound like much. But over 22 years, it adds up. And if this charge wasn’t supposed to be there, then the real problem wasn’t $47.

It was everything behind it. Sandra took the folder back to her office that evening and told Raymond she would need about 2 days to go through everything properly. Raymond agreed, but reminded her he only had 27 days left before foreclosure could begin. Sandra said she understood. And that same night, she started working.

The first thing she did was calculate the $47 fee that appeared on every monthly statement. Over 22 years, it came out to $12,408. Not nothing. But still not enough to explain a $50,000 balance. So she kept digging. She went back through older statements. 2004, 2001, even the late ’90s. Checking each one carefully.

That’s when she found the first problem. Starting in 2003, there was a second charge. Smaller, but consistent. $23 per month, labeled rural account maintenance. It showed up every month, right beside the $47 fee. Sandra checked the loan agreement again. It wasn’t there, either. Now it was $70 a month. When she recalculated everything, the total came to $27,528.

Still not $50,000. Which meant one thing. She still hadn’t found the real problem. So she kept going. And this time, she found it. Not in a statement, but in a letter from 2001. A routine account update. The kind most people would read once and forget. But inside that letter was a change. The bank had switched Raymond’s loan from simple interest to compound interest.

Sandra read that line twice. Then she ran the numbers. Over 20 years, that single change had added more than $61,000. Now everything made sense. The fees weren’t the problem. They were just the beginning. When Sandra combined the unauthorized charges with the interest change, the numbers finally lined up.

Raymond didn’t owe the bank anything. The bank had been overcharging him for years. And when Sandra applied penalties, interest on those charges, and violations under Kentucky banking law, the number changed again. This time, completely. $1.2 million. Sandra looked at the number for a moment. Then picked up the phone. It was after 2:00 a.m.

She called Raymond anyway. He answered immediately. She told him the bank didn’t have a case against him. Then she told him something even more important. He had a case against them. In that moment, everything changed. The hearing was scheduled 2 weeks later. Raymond sat at the front of the courtroom. Sandra beside him.

Across the room, the bank’s legal team looked prepared. Confident. Like this was just another case they expected to close. The bank’s lawyer spoke first. He laid it out simply. According to their records, Raymond still owed $50,000. Payment discrepancies had been identified. And under the loan agreement, the bank had the right to recover the land.

Clean. Direct. Almost routine. Then the judge turned to Sandra. She stood up, placed a stack of documents on the table, and began calmly. She explained the $47 monthly charge, never listed in the contract. Then the additional $23 fee, also not authorized. The judge followed along, turning pages as Sandra spoke.

Then Sandra moved to the interest change. She pointed to the 2001 letter, explaining how the bank had switched the loan from simple interest to compound interest without proper consent or agreement. The bank’s lawyer interrupted, saying the change had been disclosed. Sandra didn’t raise her voice. She simply clarified it had been mentioned but never agreed to, never signed, never acknowledged. The room grew quieter.

Then she presented the numbers, the unauthorized fees, the additional interest, and finally the total impact. Raymond did not owe the bank. The bank had been overcharging him for years. When she finished, the judge looked towards the bank’s side. “Do you dispute these calculations?” For the first time, the bank’s lawyer hesitated. He asked for more time.

The judge didn’t agree. “You’ve had years to review your own records.” Silence. She looked back down at the documents, then up again. “What I see here is not a simple discrepancy.” A brief pause. “It is a pattern.” The courtroom went completely still. “A pattern of charges that were never agreed to and changes that were never properly authorized.

” The bank’s lawyer had nothing to say. The judge closed the file. “The claim against Mr. Holt is dismissed.” Another pause. “And based on the evidence presented, this court finds the bank liable for the overcharges and violations. Damages will be awarded accordingly.” The number had already been calculated, $1.2 million.

Raymond didn’t react right away. He just sat there staring ahead. 22 years of payments reduced to one moment. Sandra placed a hand beside him. He nodded once. The same bank that came to take his land walked out owing him instead. Raymond didn’t win because he was lucky. He won because he paid attention. For 22 years, he trusted the system and in the end, he proved the system was wrong.

Stories like this don’t get told enough because most people don’t look close enough to see them. But once you start noticing, you can’t unsee it. If you’re still watching this, subscribe so you don’t miss the next story when it drops because once you start noticing, you can’t go back.